The Case for UK Living

It is not without irony that, as the UK approaches the 10-year anniversary of the Brexit vote, the country’s housing market is increasingly European in shape.

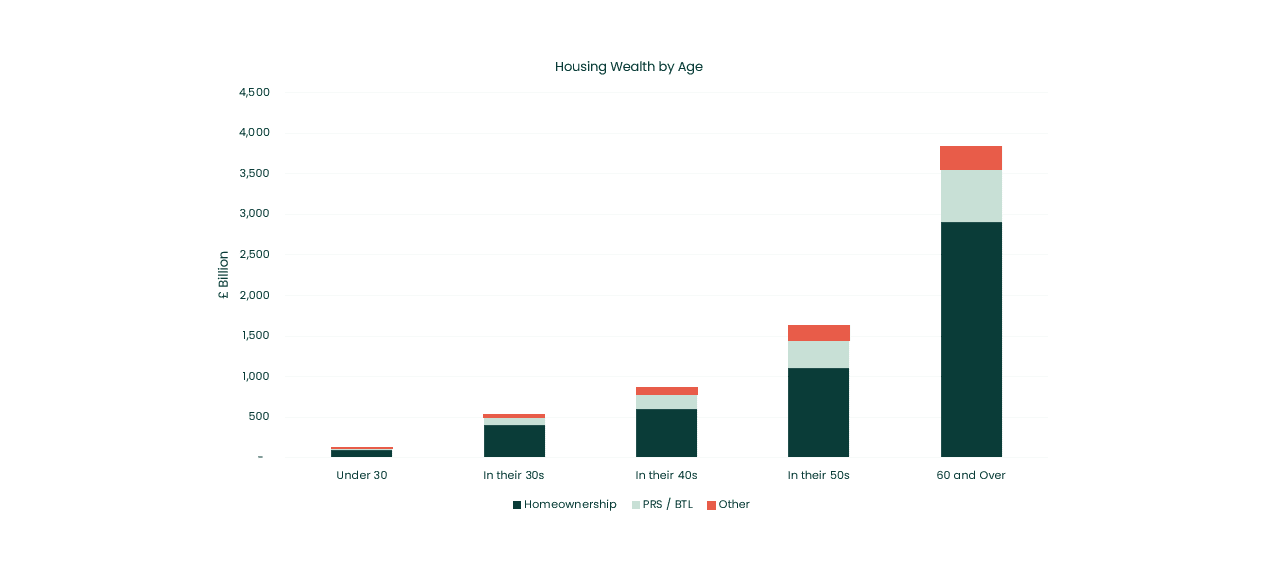

Despite popular notions of post-Thatcher Britain as an Anglo-Saxon property-owning democracy, and the idea that “an Englishman’s home is his castle”, the United Kingdom’s homeownership rate sits below that of most other European countries. Worsening affordability has been the key driver behind the fall in British owner-occupation, with inadequate supply and tighter mortgage lending pushing homeownership out of reach for many. This problem is compounded by over 55% of the owner occupier housing stock sitting with the people aged 60 and over.

“UK house prices are now 8.5x median earnings, 55% higher than in 2000.”

Office for National Statistics

Meanwhile, the arrival of the Renters’ Rights Act has created a more regulated – and more continental – private rental market, with the introduction of periodic tenancies and greater tenant rights across the board. The resulting action has been definitive, with traditional owners of this type of housing stock making a mass exodus from the market. The growth of build-to-rent, albeit representing less than 1% of residential accommodation in the UK, means many private renters now live in German-style, institutionally owned apartment blocks. Both these factors have squeezed all segments of the market significantly.

Where the UK has led the region is in the provision of modern purpose-built student accommodation. The quality of UK educational institutions has attracted international students from across the globe, many of whom are willing to pay a premium for secure, amenitised, and serviced halls of residence with professional on-site management. This has however led to upward pressures and rents, with feasibility and demand for higher education in the UK in question.

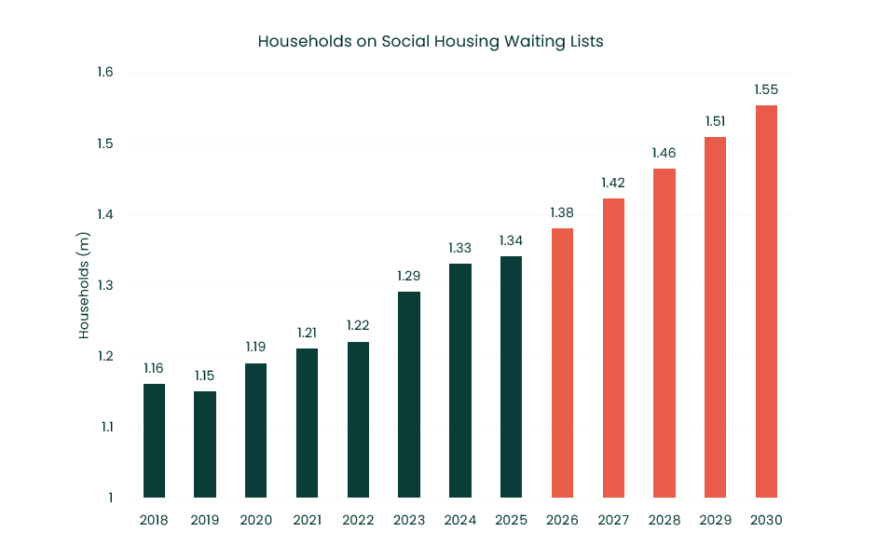

Across all housing types and tenures, the UK faces a deep shortfall that is being entrenched by worsening development viability. Increased developer obligations, taxation, and regulation, combined with reduced capital availability, are working together to undermine new delivery.

London, for example, is experiencing the city’s worst housebuilding crisis since the Second World War. Housing starts in the UK capital in 2024/25 fell to their lowest levels in over 80 years, with only 4,170 new homes starting construction in the 2024/25 financial year – a 72% drop from the previous year. The trickle down effect is meaningful, with one in four Londoners now in some kind of subsidized or social housing.

For investors able to access existing stock, there is a clear opportunity to capitalise on a widening demand-supply imbalance and secure long-term income streams with defensive, counter-cyclical, and inflation-hedging qualities.

Rental demand – whether for student accommodation, private housing, or affordable housing – typically increases during periods of recession, as consumers prioritise education and avoid significant financial commitments such as homeownership. Regardless of exactly where we are in the economic cycle, rental demand in the UK is structurally underpinned by housing unaffordability.

Looking at the current landscape, with elevated inflation concerns defining the macroeconomic outlook, the residential-for-rent sectors are increasingly attractive, given that residential rents have historically tracked inflation over the long term. Continued dislocation in capital markets also allows operational assets to be acquired on an attractive entry basis, as thinner investment volumes cloud pricing and tougher refinancing conditions create motivated sellers.

Investing in UK living offers more than just financial returns. By upgrading existing stock to meet modern energy-efficiency standards and repurposing assets to address urgent housing needs – including care, supported housing, and temporary accommodation – investors can also achieve positive environmental and social impact.

At Greenridge, we are examining opportunities in the social and affordable housing segment, where the mismatch between demand and supply is arguably greatest. The sector also offers the ability to satisfy non-financial objectives while achieving attractive returns through a derisked income profile.