Does retail favour the brave? It depends

Geopolitical instability and in particular the war in Iran will have material consequences for retail downstream. This is why a whole raft of industries expect rising inputs costs – from textiles and clothing, to haulage and agriculture – with some supply-related pressures already proving difficult to absorb.

Retail is of course no stranger to volatility. In January, we wrote of the sector’s resilience in our article, How physical retail became real estate’s prize fighter. Even in the face of an almost total (and completely unprecedented) restriction on trade in 2021, retailers proved more than capable of rapidly adapting inventory and logistical requirements to protect their businesses.

Because retail has for a lack of a better description ‘rolled with the punches’, we have no doubt, then, that retail will as a whole overcome the turbulence presented by the current macroeconomic climate, finding creative solutions to relieve constraints on margins and financing, while maintaining – and in some cases modestly growing – sales volumes.

That some investors will take a more cautious view is, as we see it, a compelling opportunity. Misreading short-term disruption as a reason to downgrade longer-term returns expectations has historically been a source of alpha at Greenridge, rewarding more contrarian, less risk-averse investment managers who have the ability to decipher the market noise.

No time to check-out

Though there may be some near-term pause in take-up while retailers let current affairs wash through, the occupational fundamentals underpinning UK retail are durable. In 2025, retail parks and shopping centres outperformed all-property industry benchmarks, supported by the slow unwinding of a Pandemic-induced contraction in physical footprint.

This is reinforced by favourable supply-side dynamics. New development being cyclically and to some extent structurally limited by rising construction costs and a restrictive planning system, concentrating demand in a pool of existing high-quality stock that is itself shrinking.

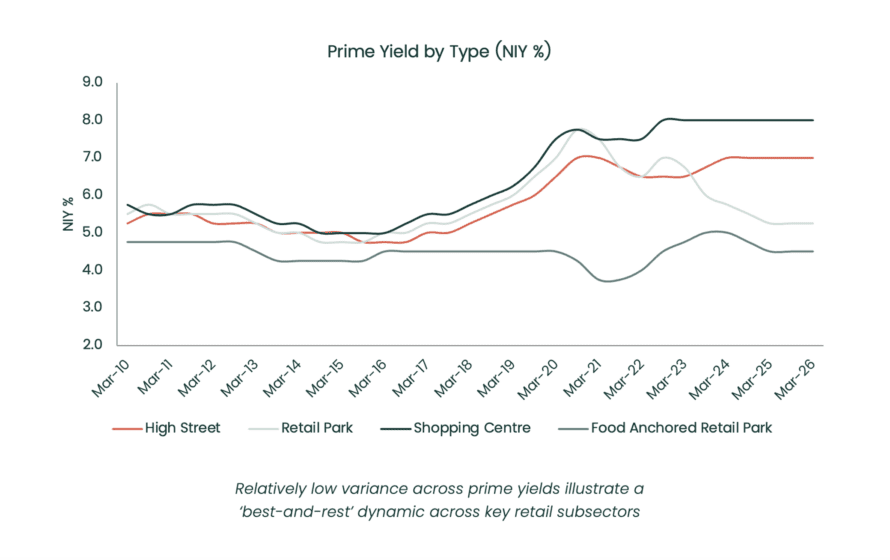

In an income-led cycle, where investors are focused on the quality of their cashflows in the absence of yield compression, these features take on an outsized importance. In the last 12-to-18 months we have seen rental growth across prime shopping centres banding 3.5%, its highest level since 2006, at the same time as consumer spending has stabilised.

Building exposure to the bulls-eye zone

Retailers use the term ‘bulls-eye zone’ to describe the shelf space at a customer’s eye level – the position that captures attention and commands a premium. Investors in retail real estate must apply this same discipline, recognising that this sector is both highly polarised and extremely competitive.

Prime and best-in-class assets will continue their trend of outperforming across sectors, with prohibitive development economics and capital availability underscoring rental growth over the medium-term. Defensive segments such as retail parks and supermarkets are a different animal, with performance depending on the quality of covenant, co-location opportunities, and value creation through active asset management – something Greenridge has been doing for over three decades.

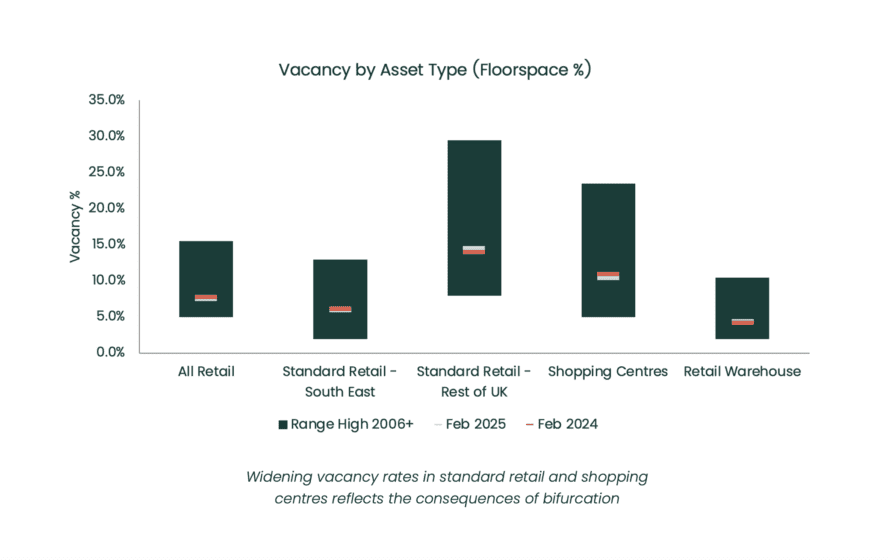

By contrast, in secondary locations, the bulls-eye zone is extremely narrow. Hyperlocal knowledge in these sub-markets is essential in unlocking value, to avoid the punishing consequences of bifurcation driven by the rebalancing efforts of large retailers that are shedding surplus retail floor space either to redeploy in prime locations and in more popular retail formats, or as part of cost mitigation strategies.

Selectivity is key

Much like in the immediate aftermath of Covid-19, capitalising on relative value in this choppier period for retail is a function of impatience, conviction, and selectivity. Environments like these often reward the contrarians that combine creative financing with versatile, hands-on asset management capabilities, whether that is in dealmaking or when investing in existing assets.

Selectivity is, however, essential. Though retail has historically favoured the brave, it is a sector that is becoming more competitive, and more nuanced. Despite strong fundamentals, a bifurcated and uncertain market magnifies the losses, as well as the wins. Making it all the more important that managers intimately understand the granular dynamics of the sector from the inside-out.