The benefits of underwritten income in a world of uncertainty

The current investment landscape is increasingly fragile, it is defined by elevated equity valuations, compressed forward returns, and a structural breakdown in traditional stock–bond diversification. Within this context, different asset classes serve distinct structural roles: growth assets create upside; defensive assets protect downside. In this environment, portfolios need more than just growth and defence, they need reliability and this is where underwritten income comes in, creating structural stability when other assets cannot.

The term “underwritten income” describes a rental income stream that is contractually secured at the asset level through a combination of lease structure, tenant creditworthiness, and physical asset quality. It is the distinguishing characteristic that differentiates income-led commercial real estate from a generic “high yield” allocation.

Predictable income has become one of the scarcest and most valuable attributes a portfolio can possess. However, not all income is equal.

Public market income – dividends from equities, coupons from bonds – is repriced daily and subject to discretionary cuts, credit events, and reinvestment risk. By contrast, commercial property income can be contractually underwritten: secured by long-dated leases with defined terms, indexed uplifts, and the covenant strength of institutional-grade tenants.

As investors navigate compressed risk premia, unstable correlations, and heightened geopolitical complexity, our belief remains that income-led commercial real estate offers cashflow visibility, downside cushioning, and portfolio efficiency benefits that are difficult to replicate through conventional asset classes.

UK commercial property leases are legally binding contracts specifying rental amounts, payment frequency, lease duration, break clauses, and review mechanisms. Unlike equity dividends, which boards may reduce or suspend at their discretion, contracted rent is a legal obligation of the tenant. The landlord’s right to receive income is secured by the lease and, ultimately, by the physical asset itself.

Income durability cushions valuation volatility. During the 2022–2024 real estate downturn, UK property values fell by around 25%, yet rental income in certain sectors, such as industrial and logistics, continued to grow.

Contractual income from well-underwritten commercial property is not a substitute for equities or bonds, but a complement – a third structural pillar that provides the predictable cashflow, low correlation, and inflation-linked growth that neither equities nor fixed income can reliably deliver in the current macro-regime. Contractual income, properly underwritten and conservatively structured, provides a structural advantage for investment portfolios that transcends market cycles and rewards the patience of long-term capital.

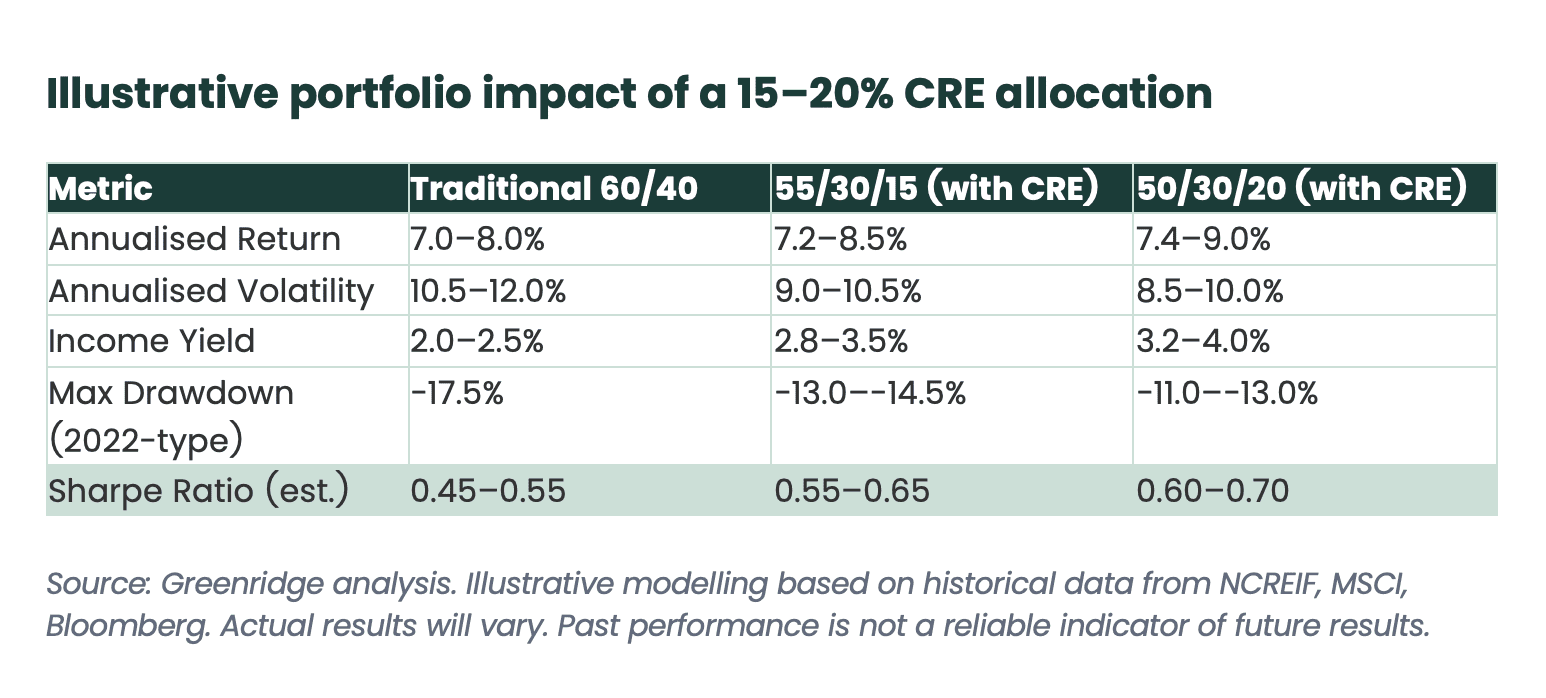

The current market environment favours income-led strategies over capital-growth strategies. Property yields have seen little to no compression in 2025 and Capital Economics expects stability to continue. With 10-year gilt yields around 4.25%, the spread between property income yields and risk-free rates remains attractive, particularly for investors deploying conservative leverage to enhance income returns.

Academic and institutional research consistently identifies a 10-20% portfolio allocation to private real estate as the range that optimises diversification benefits without excessive illiquidity. Within this range, income-led strategies should form the core, supplemented by selective value-add or opportunistic plays where appropriate.

Investors should prioritise opportunities exhibiting the following attributes: strong tenant covenants (investment-grade or equivalent); long WAULTs (eight years or above to expiry); conservative loan-to-value ratios (below 55–60%); assets in established, liquid sub-markets with strong occupier demand; and lease structures incorporating indexed or fixed rent reviews to provide inflation protection.

We will be exploring these themes in more detail in a forthcoming whitepaper and although we are talking specifically about underwritten income in this blog, we will be explaining how our stock selection and investment process have allowed Greenridge to benefit from all three pillars of returns; growth, structural stability and defensible positioning in volatile markets.