A generational opportunity in UK regional offices

After years of negative headlines, a compelling demand-supply story that is delivering positive rental growth has started to lure global capital back into the UK office market. This can be seen even in the regions, where investment volumes hit £3.6 billion in 2025 – a 23% increase on the total recorded in 2024 – according to Savills.

To date, the main buyers have been private capital, be that family offices or North American fund managers. The same Savills research suggested institutional buyers accounted for just 4% of investment volumes in 2025 – the lowest proportion in over a decade.

However, as prime rental growth continues to power ahead, reaching 10.2% growth across the ‘Big Six’ (Birmingham, Bristol, Edinburgh, Glasgow, Leeds and Manchester) according to LSH, we expect institutional capital to increasingly target regional office opportunities in the UK in search of diversification and yield.

As Knight Frank notes, prime office yields across the UK regional cities, ranging from 6.50% in Edinburgh, 6.75% in Birmingham, Bristol and Manchester, 7.50% in Glasgow, Newcastle, and Sheffield, to 10% in Aberdeen, represent a substantial premium to London benchmarks. By comparison, yields stand at around 5.25% in the City and 3.75% in the West End, highlighting “the strong relative value available outside the capital.”

“At Greenridge, we see there being a fast-closing buying window to take advantage of a generational arbitrage opportunity in regional offices before institutional money fully re-enters. Improving take-up in core US office markets, which often acts as a bellwether for capital flows, will see investor sentiment towards offices improve, further encouraging institutions to re-allocate to the asset class.”

Paul Simmons

In the UK, regional office pricing still reflects a cautious outlook despite improving occupational fundamentals and for now, rents per square foot still sit below the levels needed to justify speculative development, limiting future supply. This scenario will likely not last forever. Indeed, CBRE is already forecasting competition for grade A space could push rents in some regional cities towards £55.00 per sq. ft. – around the level needed to “justify the start of a new speculative development cycle.”

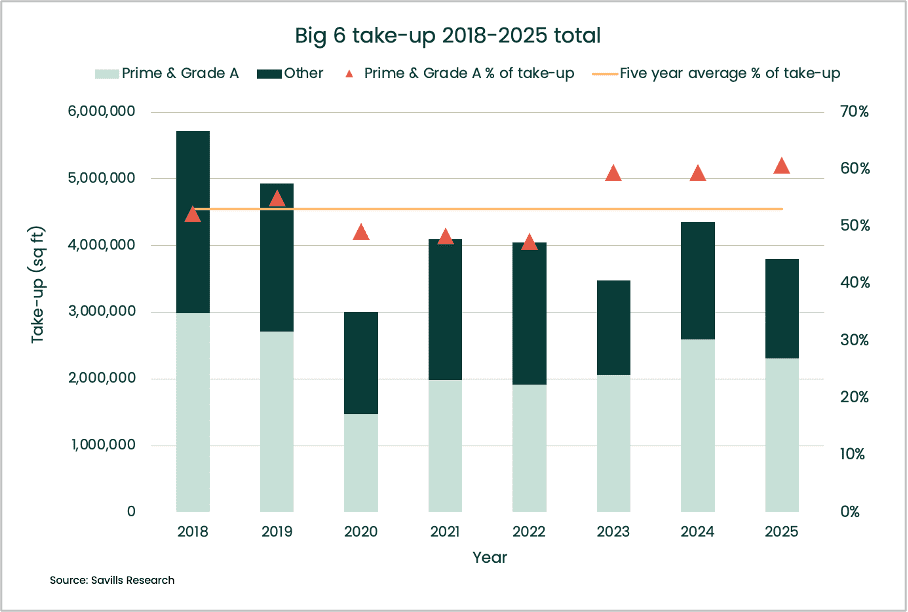

Regional office stock has already contracted by around 4% on average, driven partly by changes of use, typically to residential but also hotels, and the removal of secondary space from the market. At the same time, occupier demand continues to concentrate in best-in-class space. Last year, Grade A and prime offices accounted for approximately 60% of regional take-up, highlighting what has to date been a “flight to quality”.

Secondary offices are facing rising incentives, falling effective rents, and mounting obsolescence risk. Hybrid working, ESG requirements, EPC ratings, and technological change are accelerating the concentration of demand in major hubs, leaving non-core offices increasingly challenged.

Demand is increasingly concentrated among larger, well-capitalised occupiers (often multinational businesses) who are rationalising portfolios and upgrading into best-in-class space, rather than expanding footprints. This “flight to quality” is now feeding through into regional markets, where supply of modern, sustainable offices remains limited and older stock continues to fall out of favour.

The disconnect between capital markets and occupational markets offers savvy investors a clear opportunity to secure high-quality, yet fundamentally mispriced, assets, in core locations that will be highly sought-after by institutions once they fully re-enter.

Our belief is that regional markets are at an earlier stage of repricing than London and will follow the UK capital in seeing an office revival. Historical trends reinforce this thesis, with a similar dynamic having played out in the aftermath the great financial crisis. You can already see the London-to-regions trend in the occupational market, and where occupiers lead, capital follows.

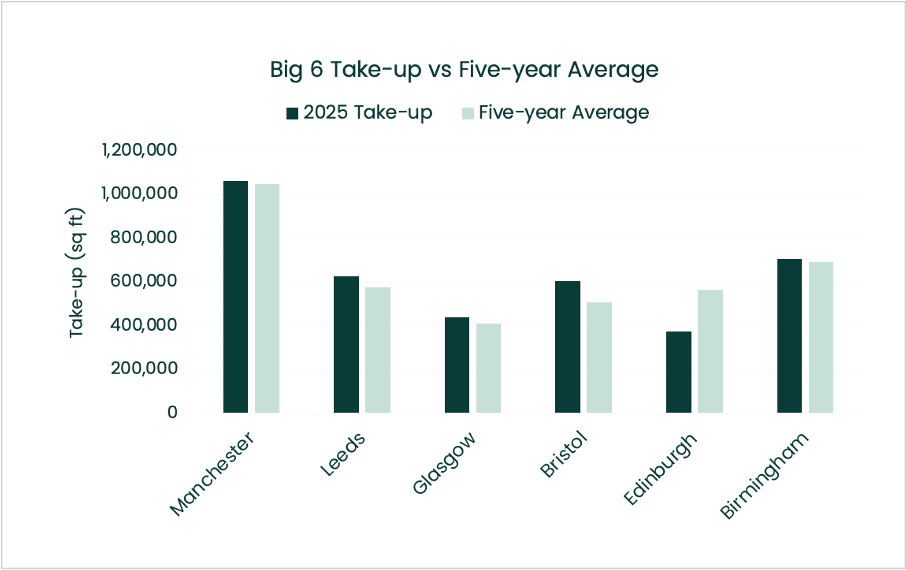

Manchester, Leeds, Glasgow, Bristol and Birmingham exceeded their five-year average take-up levels in 2025. The legal sector, which helped drive the recovery of central London office take-up, has been behind some of the landmark leases in core regional cities. Notable examples include Eversheds taking over 47,000 sq ft at 1 Crown Point Road in Leeds in Q3 last year, while fellow law firm Pinsent Masons agreed Scotland’s largest transaction, taking nearly 32,000 sq ft at Aurora in Glasgow.

However, the opportunity set in UK offices is far greater than simply buying best-in-class for what is historically cheap, with regional offices valued at close to 40% below than their mid-2022 peak. There is a growing opportunity to repurpose and reposition existing assets, particularly where embodied carbon considerations make refurbishment a more attractive and sustainable alternative to new development. Lower-quality and more peripherally located assets (particularly those capable of being upgraded to meet modern occupier and ESG requirements) stand to benefit from occupiers widening their search as prime rents continue to race ahead, pricing out a greater variety of firms.

CBRE is predicting tight grade A vacancy rates in core locations, as well as an increased focus on cost, “will shift many large occupiers’ requirements towards good quality space in more peripheral locations, ending the domination of ‘flight to core’.” Identifying what secondary stock can reasonably be positioned to attract high-calibre occupiers, whether through refurbishment, reconfiguration or improved sustainability performance, requires a granular understanding of property-level dynamics – a skillset we have developed over our three decades-plus of buying and managing UK commercial real estate.

At Greenridge, we’ve already translated our conviction in regional offices into action, most notably through the acquisition of 3 Temple Quay, a prime-located Category B office scheme, from M&G Real Estate last year. With financial support from Investec, we are committed to improving both sustainability outcomes and tenant experience with a full-scale refurbishment.

As institutions look to return to the regional office investment market with one hand while continuing to offload assets with the other, we see no better time for buying than now. By establishing first-mover advantage in UK regional offices, we believe we can achieve enhanced returns without a corresponding increase in risk, as early entrants like us are best positioned to secure the most attractive assets and establish a foothold ahead of later market competition.