Are investors in real estate skim reading UK labour statistics?

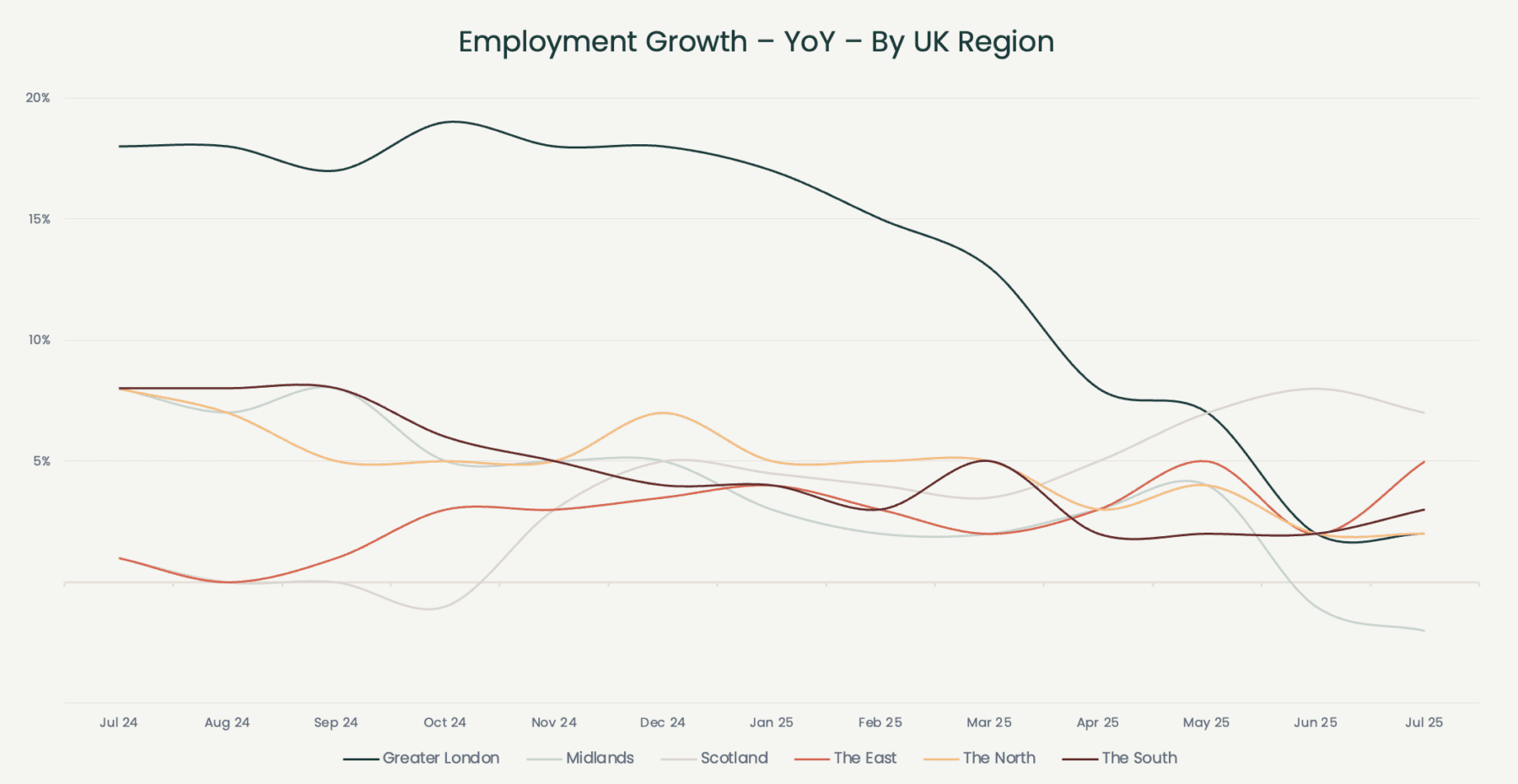

Workforce formation in the UK is a mixed picture, with unemployment in London rising to 7.6% at the end of 2025. Labour productivity is growing at a much faster clip than job creation, which some are calling a “jobless economic expansion”. But is this the full story, or the synopsis of something more nuanced?

Though we all fall prey to reading the executive summary and glossing over the detail, in the case of UK labour statistics, conflating what’s happening in the capital with the situation in the regions masks significant trends. The uncertain effects of AI are at least partially to blame, but beneath the headline estimates are obscurities. Labour markets are, in fact, tighter and are in some cases expanding in regional towns and cities.

ONS figures in the three months to December 2025 illustrates this resilience, with employment rates in the South East, South West, East Midlands, and Scotland, all outmatching London. Failing to read into seeming divergences therefore underestimates the durability of occupational markets, and therefore the yield derived on income-generating regional stock in sub-sectors such as office, retail, and leisure.

By contrast, while regional opportunities therefore represent the structural relationship of workforce expansion, vacancy, and rents, what of London? What is being ‘skim read’ there? In our view, in the office sector in particular, it is concentration. With employers in the UK willing to pay a roughly 14% wage premium for AI-skilled roles, shifting labour dynamics and the ‘known unknowns’ of AI will intensify demand for high-quality, well-connected and amenity-rich real estate to entice fresh talent.

At Greenridge, our portfolio and approach to core and non-core opportunities reflects this variation. Strategic UK assets such as One Tower Bridge in London, a mixed-use leisure and retail hub with 14 commercial units anchored by well-known occupiers and 86% of rental income index-linked, exemplify properties with desirable location, strong occupier bases, and income resilience.

Similarly, in our regional portfolio, holdings like 3 Temple Quay in Bristol and Meridian Leisure Park in Leicester demonstrate an emphasis on location quality and tenant diversity, recognising that regional opportunities are at least partially mispriced by the generalisation of labour workforce trends and the buoyancy of regional submarkets, despite regional markets providing robust groundwork for income at different tenors.

Whether AI-driven productivity gains in London or workforce participation in the regions broaden or plateau, the implication for commercial real estate is the same. Complacency is the real risk. Strengthening the case for partnerships with investment managers with deep-rooted, granular knowledge of geographic and temporal subtleties that go unnoticed at the macroeconomic level.

Labour statistics are of course one example of where the market ‘tale’ hides the long ‘tail’ of dealmaking. With coverage of key markets that connects workforce statistics with other indicators of income durability, such covenant strength, demand/supply dynamics, and barriers to entry, through sourcing to execution, a panoramic view of UK real estate is – we believe – the only means of identifying value.