How physical retail became real estate’s prize fighter

E-commerce forced a transformation in bricks-and-mortar stores that continues to define performance today.

If you were ever going to train to become a world-class boxer, you could probably learn a thing or two from physical retail. Being the real estate sector that has arguably spent the most time on the canvas over the last half-decade or so, its resilience and more recent recovery embodies the iconic line that “it ain’t about how hard you hit. It’s about how hard you can get hit, and keep movin’ forward.”

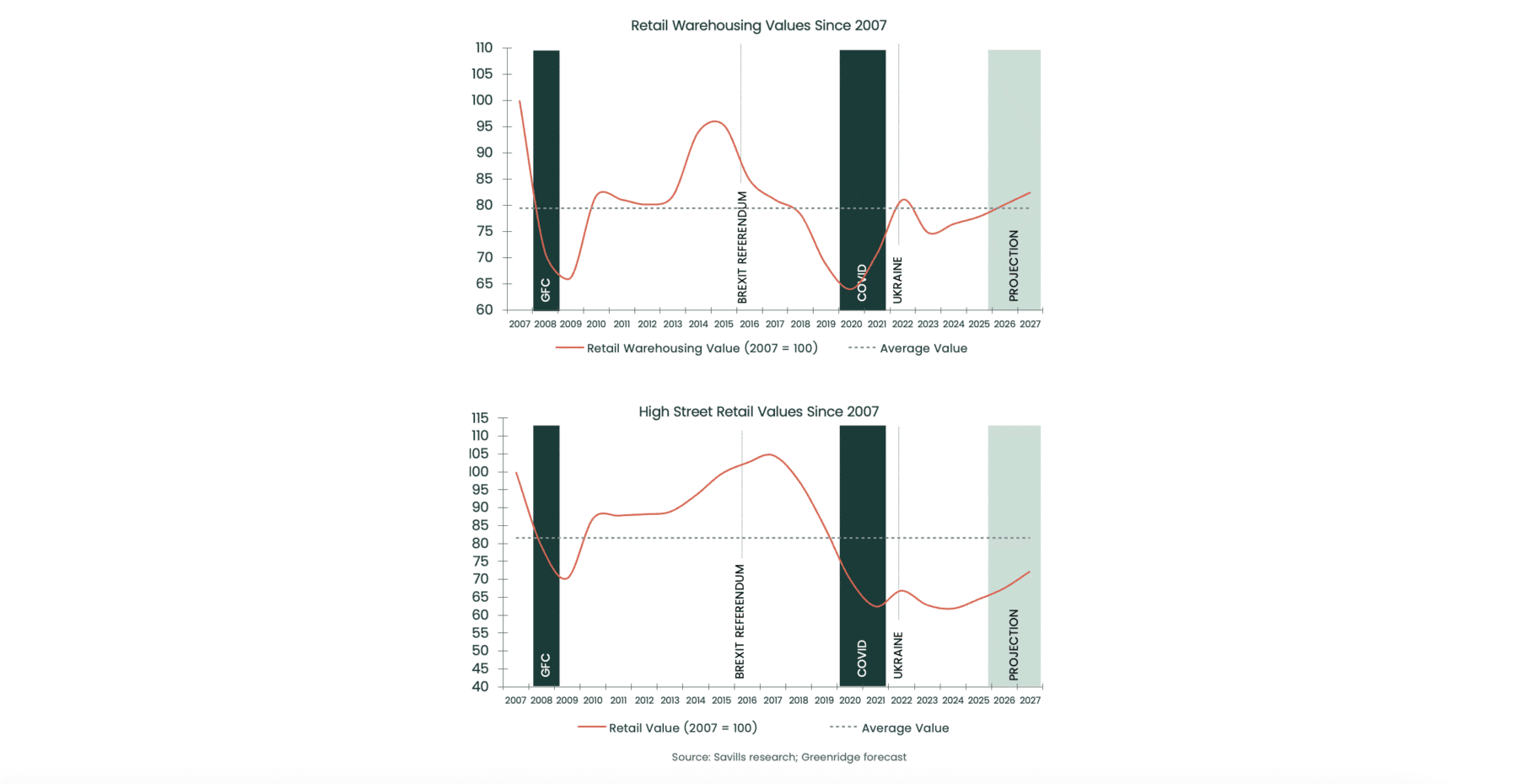

Given that physical retail has recovered at such a pace despite being forced in a pandemic to shutter stores, it should underscore why retail property deserves its place as a fixture of a balanced portfolio. Moreover, the Covid-19 era isn’t the only example of retail being ‘written-off’. In the late 1980s, when teleshopping became a thing, the growth of the then-$2.5bn industry dominated by the likes of QVC and HSN led some analysts to believe that bricks-and-mortar stores would be functionally redundant.

Of course, innovation of, and access to, online shopping has reshaped the role of physical retail and, in the process, toppled some big beasts that were once household names. Price transparency has been the biggest sucker punch dealt by e-commerce, leveraging lower operating costs to insulate from margin compression.

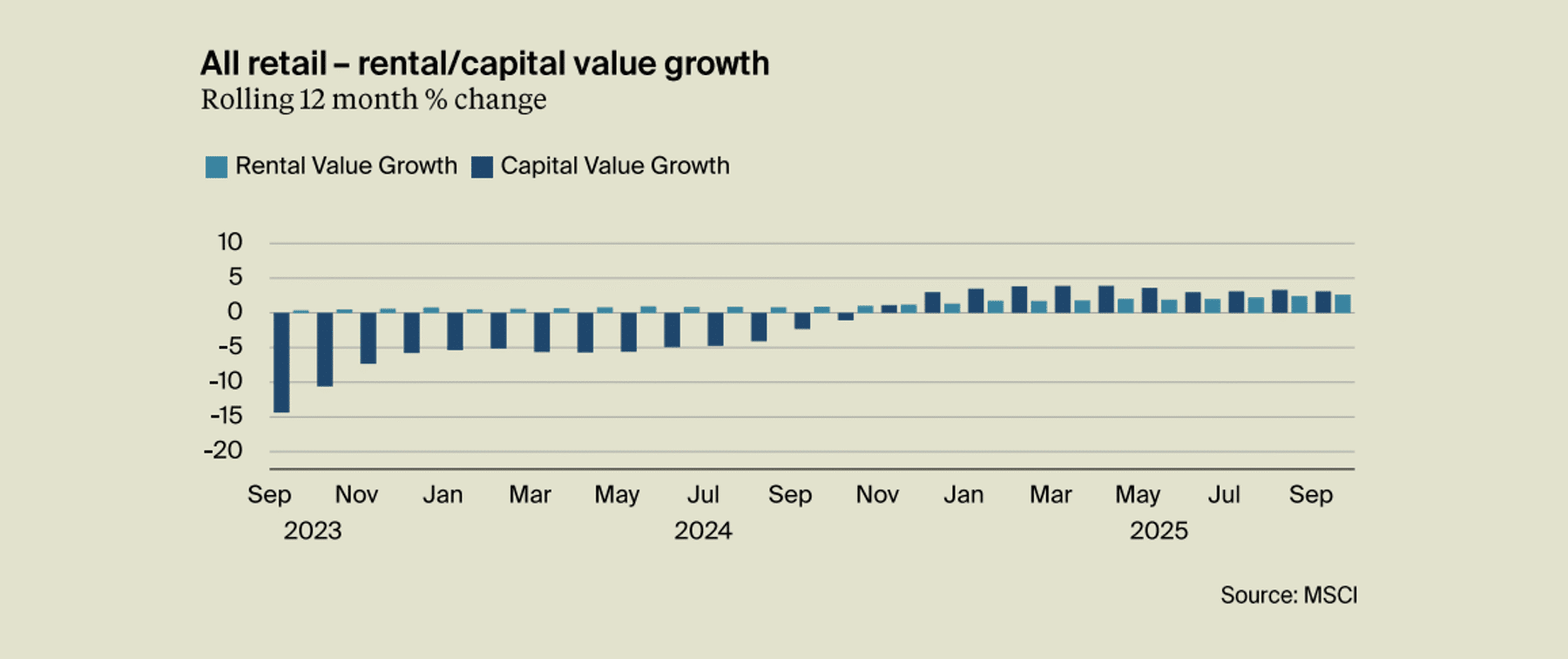

For several reasons, however, these existential threats to physical retail have helped the asset class undergo a form of accelerated maturity, evolving to remain relevant in the face of technological change. This bears out in research from Knight Frank, which suggests retail outperformed all traditional property segments in 2025, with retail expected to deliver total returns of c. 9.5% in 2026 as investor confidence rebounds.

In our experience as long-term investors in both retail parks and high street retail, this is an asset class that is more than capable of the long fight. In the challenges it has faced, operators have recalibrated everything from their store formats to inventory and warehouse management at speed to remain relevant as consumption patterns have changed. This ranges from the reinvention of ‘experience-led’ retail to differentiate from e-commerce to an enhanced focus on convenience, services, and proximity to the consumer.

As well as an improving occupational environment, e-commerce penetration is beginning to lose steam with recent figures tentatively indicating that it has reached a ‘saturation point’ in the region of 28-30% of total market share. This marks what we believe is a watershed moment for physical retail in the UK. Precipitating long-term recovery in capital values, in addition to durable rental income with lower volatility.

Investors seeking an entry point or opportunity to scale in this asset class must be aware of its idiosyncrasies. For one, the asset class has a broad definition but in fact encompasses a range of retail formats with drastically different performance characteristics, ranging from retail parks and warehousing to shopping centres, roadside retail, and high street.

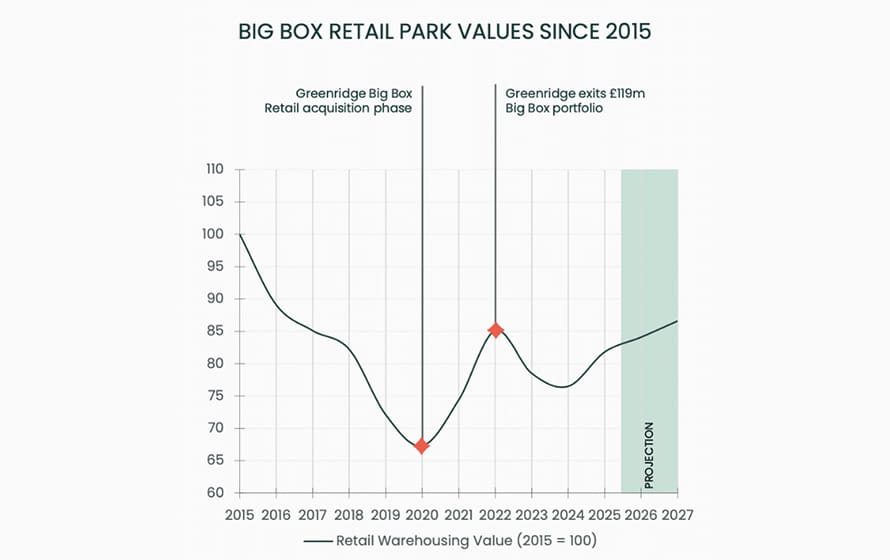

Within each subsector, there is further disaggregation by location and occupier density, and local dynamics, such as competition, that need to be factored in and balanced. In the retail park space, for example, Greenridge seeks out assets with a history of attracting established multiples with generally solid covenant strength underpinned by consistent earnings, in which opex potential exists beyond a traditional yield and covenant play to enhance value or expand income streams.

By contrast, in the case of prime high street, what we are looking for is dictated more by the brand mix and the intention of occupiers, who may be taking up a lease for brand recognition and visibility, as well as vending. Meaningful value creation at this end of physical retail therefore leans more towards lease negotiation and agglomeration benefits, as well as what differentiates an asset.

For the UK, at least, the ongoing ‘regionalisation’ of once city-centric occupiers may be the next evolution of physical retail. There may also be less obvious drivers of value, such as cyber threats to e-commerce platforms that recentre confidence in physical retail.

In whichever scenario it may be, we remain of the view that physical retail, in its proven resilience and if approached selectively, has the potential to be an enduring area of opportunity for real estate investors seeking reliable alpha in this phase of the cycle.